Phoenix Roof Insurance Claims: What Adjusters Actually Look For (and Your Rights Under AZ Law)

How Phoenix roof insurance claims really work — what adjusters inspect, ACV vs RCV, monsoon wind/hail deductibles, Arizona ROC verification, and homeowner rights under AZ insurance code.

Phoenix Roof Insurance Claims: What Adjusters Actually Look For (and Your Rights Under AZ Law)

TL;DR for Phoenix Homeowners

A Phoenix roof insurance claim is won or lost long before the adjuster shows up. Carriers in Arizona increasingly distinguish between sudden, accidental damage (covered) and gradual wear-and-tear (excluded), apply separate percentage deductibles for wind and hail, and pay Actual Cash Value (ACV) rather than Replacement Cost Value (RCV) on older roofs. Adjusters look for specific failure signatures — directional bruising, fresh granule loss, splatter patterns, lifted tile courses — and they document everything. Your rights under Arizona Revised Statutes Title 20 include a written denial explanation, a prompt response timeline, and recourse through the Arizona Department of Insurance and Financial Institutions if a carrier acts in bad faith. Before filing, document the roof in pre-storm and post-storm photos, verify your contractor at the Arizona Registrar of Contractors, and read the wind/hail endorsement on your declarations page.

Why Phoenix Roof Claims Are Different

A roof claim in Phoenix is not the same financial event as a roof claim in Tampa or Tulsa. Two factors reshape the math.

First, the storms are concentrated. The National Weather Service Phoenix Forecast Office defines the Arizona monsoon as June 15 through September 30, with most damaging wind and hail events compressed into a handful of microburst-driven afternoons (source: NWS Phoenix monsoon information). When a microburst dumps 60–80 mph gusts across a neighborhood, carriers see hundreds of claims filed against the same storm — and they staff up adjusters and tighten scrutiny accordingly.

Second, the roofing inventory is unusual. Concrete tile dominates Phoenix tract housing built after the late 1980s. Tile roofs do not fail the way shingle roofs fail; the tile itself often outlasts the homeowner, while the underlayment beneath silently exhausts after 15–25 years. Adjusters trained on shingle-belt loss patterns sometimes misread tile-roof damage entirely, and homeowners frequently file claims for what is actually age-related underlayment failure — which is never a covered loss.

Understanding the carrier's playbook before you file is the difference between a paid claim and a denied one.

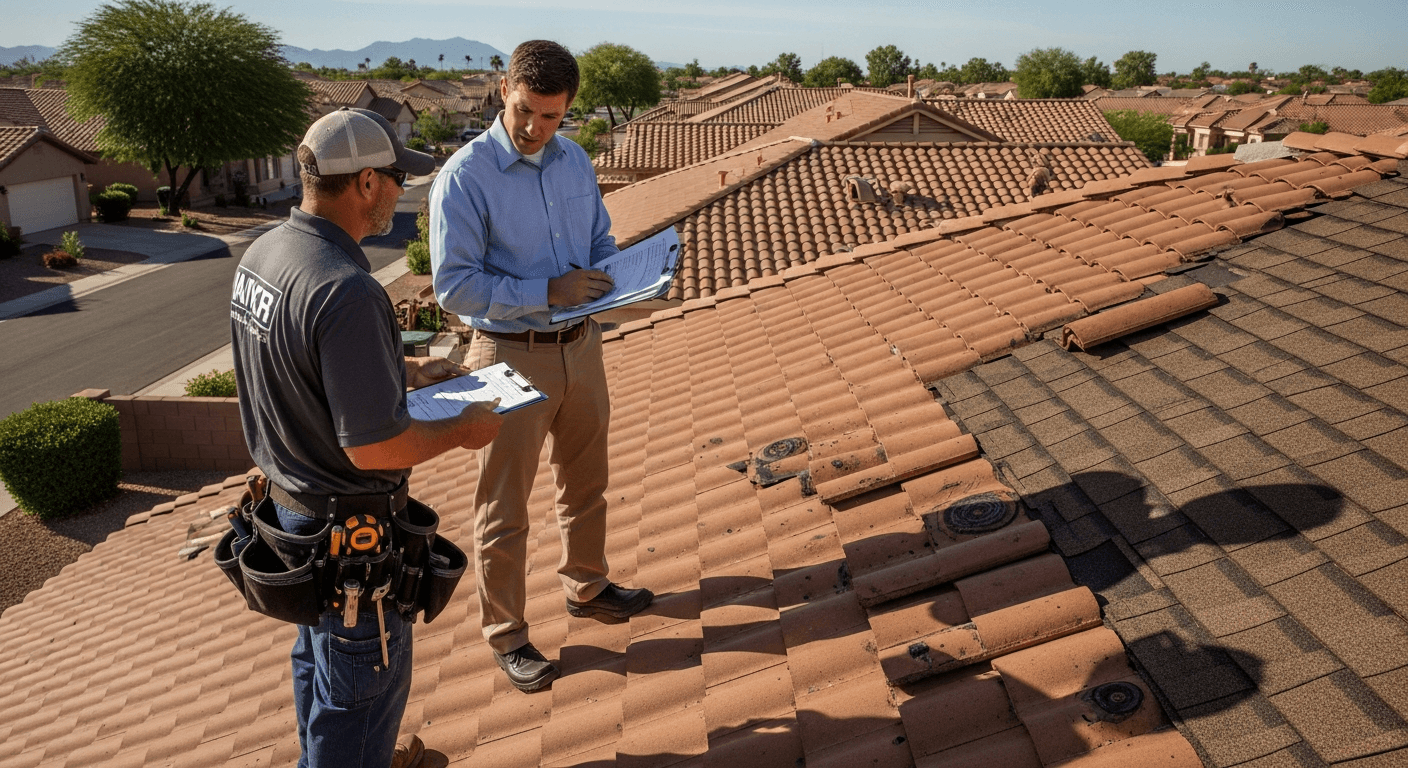

What Adjusters Actually Look For on a Phoenix Roof

An adjuster's inspection is a structured forensic exam, not a casual walkaround. Here is the sequence most Arizona field adjusters follow, and what each step is meant to prove or disprove.

1. Storm-date causation

The adjuster's first job is to determine whether the damage is consistent with a single, recent, covered event — or whether it is the cumulative result of years of UV exposure and thermal cycling. They will cross-reference the date you reported the storm against NOAA storm reports, local NWS storm event archives, and CoreLogic or HailVerify hail-swath data. If your claimed damage doesn't match a documented storm within a reasonable window, the claim is at high risk of denial.

This is why prompt notification matters. Most Arizona policies require notice "as soon as practicable" after a loss. The Insurance Information Institute notes that delayed reporting is a leading reason carriers cite when contesting storm-damage claims nationally (source: III Facts + Statistics: Homeowners and Renters Insurance).

2. Damage signature — wind

For wind damage, adjusters look for:

- Directional patterns — damage clustered on the windward (typically south or west) face, with the leeward face untouched, is a signature of a discrete wind event.

- Creased shingles — shingles that were lifted by a gust, folded back, and then dropped. The crease line is a fingerprint of wind uplift.

- Missing tabs or full shingles with intact, undamaged fasteners still in the deck — meaning the shingle pulled off the nails, not that the deck failed.

- Lifted or slipped tile courses, especially at hips, ridges, and rake edges where wind pressure concentrates.

3. Damage signature — hail

Hail damage is more subjective than homeowners realize. Adjusters look for:

- Bruising on asphalt shingles — soft spots where the mat has been fractured beneath an intact granule surface. Found by feel, not by sight.

- Granule loss in circular patterns roughly the diameter of the reported hailstone size, exposing the black asphalt mat.

- Splatter marks on metal flashings, vent caps, and HVAC fins — independent corroborating evidence that hail actually hit the property.

- Cracked or shattered tiles with fresh fracture edges (not weathered or dirty).

A claim filed for "hail damage" with no splatter marks on metal and no fresh granule loss in downspouts is treated skeptically.

4. Wear-and-tear flags

Adjusters are trained to spot — and document — wear-and-tear conditions that are not covered losses. The big ones in Phoenix:

- Heavy uniform granule loss across the entire roof field (UV degradation, not storm damage)

- Edge curling and cupping on shingles (thermal cycling)

- Chalky white surface on foam roofs (coating failure overdue for recoat)

- Brittle, exposed underlayment on tile roofs (age, not event)

- Corroded fasteners and rusted flashings without storm-related impact

If the adjuster's report describes any of these, expect the claim to be reduced or denied for those areas.

5. Roof age and prior repairs

The adjuster will ask — and verify against permit records — how old the roof is and what prior repairs have been done. A patched roof with mismatched shingle generations or multiple layers of coating tells a story that affects both coverage and valuation.

ACV vs RCV: The Single Most Important Line on Your Policy

The biggest financial swing in any Phoenix roof claim is whether the carrier pays Actual Cash Value (ACV) or Replacement Cost Value (RCV).

RCV pays what it costs to replace the roof today, with no deduction for age. You get a check for the actual rebuild cost (minus your deductible).

ACV pays the depreciated value of the roof — replacement cost minus accumulated wear from age. A 20-year-old asphalt shingle roof with a $16,000 replacement cost might pay only $4,000–$6,000 on an ACV basis, leaving the homeowner to fund the difference.

Arizona carriers increasingly apply ACV — often called a "roof endorsement," "roof settlement schedule," or "matters of age" endorsement — to roofs older than 10 or 15 years, with the depreciation curve specified in the policy. The National Association of Insurance Commissioners has tracked the growth of these endorsements in catastrophe-exposed states throughout the 2020s (source: NAIC consumer information on homeowners insurance).

Read your declarations page and endorsement list. If you do not see "Replacement Cost — Roof," assume ACV applies. If it matters, talk to your agent at renewal — not after a storm.

The Wind/Hail Deductible Trap

A standard Arizona homeowner policy might show a $2,500 all-perils deductible on the declarations page — but bury a separate wind/hail deductible in the endorsements, expressed as a percentage of the dwelling coverage limit rather than a flat dollar amount.

On a home with $400,000 in dwelling coverage:

- A 1% wind/hail deductible = $4,000

- A 2% wind/hail deductible = $8,000

- A 5% wind/hail deductible = $20,000

The Insurance Information Institute documents that percentage deductibles for wind and hail are now standard practice in most catastrophe-exposed regions of the United States (source: III Hurricane and Windstorm Deductibles). Many Phoenix homeowners discover their wind/hail deductible only after a monsoon claim, when the carrier sends a settlement letter showing a five-figure deductible they didn't know they had.

"The biggest 'gotcha' we see on Phoenix monsoon claims isn't the damage assessment — it's the deductible. A homeowner files for $9,000 in wind damage thinking they owe $2,500 and finds out they owe $8,000. The claim was valid; the math just didn't pencil out. Always read the wind/hail endorsement before storm season." — Senior estimator, Phoenix-area roofing inspection practice (paraphrased from intake notes, 2026)

Your Rights Under Arizona Insurance Law

Arizona Revised Statutes Title 20 governs the insurance industry in the state, and several provisions specifically protect homeowners during the claim process.

Prompt response timeline

Under ARS Title 20, Chapter 2, Article 7 (the Arizona Unfair Claims Settlement Practices Act), carriers must acknowledge a claim within a reasonable time after notice, complete an investigation within a reasonable time after notice, and pay or deny within a reasonable time after they have what they need to decide. The Arizona Department of Insurance and Financial Institutions (DIFI) publishes consumer guidance on what counts as reasonable and how to file a complaint when a carrier drags its feet (source: Arizona DIFI consumer assistance).

Written denial explanation

If your claim is denied in whole or in part, you are entitled to a written explanation citing the specific policy provisions the carrier is relying on. "Wear and tear" alone is not a sufficient denial — the carrier must point to a policy exclusion and explain how it applies to your specific facts.

Right to appraisal

Most Arizona homeowner policies include an appraisal clause that lets either party — you or the carrier — invoke a binding appraisal process when there is a dispute about the amount of loss (not coverage itself). Each side picks an appraiser; the two appraisers pick an umpire; their decision is binding. This is faster and cheaper than litigation and is underused by homeowners who simply accept the carrier's initial estimate.

Right to file a DIFI complaint

If you believe the carrier is acting in bad faith — slow-walking the claim, lowballing the estimate, misrepresenting policy terms — you can file a complaint with the Arizona Department of Insurance and Financial Institutions. DIFI does not adjudicate your claim, but it does open a regulatory file with the carrier, and that often triggers a more serious internal review.

Right to your own public adjuster

You may hire a licensed public adjuster to represent your interests against the carrier. Public adjusters in Arizona must be licensed by DIFI and are typically paid as a percentage of the settlement. For large or complex claims, this can be worthwhile; for small claims, the percentage fee may eat too much of the recovery.

Verifying Your Contractor: The Arizona ROC Step Homeowners Skip

The single most expensive mistake on a Phoenix roof claim is hiring an unlicensed contractor. The Arizona Registrar of Contractors (ROC) licenses roofing contractors under several classifications, and unlicensed work above the $1,000 small-job threshold violates Arizona Revised Statutes Title 32, Chapter 10 (source: Arizona ROC contractor search).

The consequences cascade:

- Insurance denial. Carriers can deny coverage on covered losses when work is performed by an unlicensed contractor.

- No ROC recourse. If the work is defective, the ROC's Residential Contractors' Recovery Fund (which can pay up to a statutory cap on judgments against licensed contractors) does not apply to unlicensed work.

- Permit refusal. Municipal building departments will not issue permits to unlicensed contractors, meaning the work is not inspected and may not pass when you sell the house.

- No mechanic's lien protection that runs both ways. The full legal framework that governs licensed contractor-homeowner relationships in Arizona depends on the license being valid.

Verify every contractor at the ROC's public license search before signing anything. Confirm the license is active, the classification covers roofing work, and there are no recent disciplinary actions. Also ask for a Certificate of Insurance showing general liability and workers' compensation — and verify it directly with the insurance carrier, not just by glancing at a PDF.

A Pre-Claim Checklist for Phoenix Homeowners

Before you call the carrier:

- Document the damage with date-stamped photos from multiple angles, including overall roof shots and tight close-ups of specific damage signatures.

- Find your pre-storm photos if you have them — Google Street View, real-estate listing photos, prior inspection reports — and compare.

- Pull your declarations page and endorsements and confirm your wind/hail deductible amount, your ACV vs RCV status, and any roof age limitations.

- Get one ROC-licensed contractor estimate in writing with a detailed scope of work before filing, so you have an independent baseline number.

- Calculate whether the claim is worth filing. If the damage estimate is close to your wind/hail deductible, filing may hurt you more than help (carriers track claim frequency and may non-renew).

- File with prompt written notice, retain a copy of everything you send, and request a claim number and assigned adjuster name in writing.

Frequently Asked Questions About Phoenix Roof Insurance Claims

Will my Arizona homeowner's policy cover monsoon roof damage? Wind and hail damage from a monsoon storm is typically covered, subject to a separate wind/hail deductible that is often expressed as a percentage of the dwelling coverage amount. Wear-and-tear, cosmetic damage, and pre-existing conditions are not covered.

How long do I have to file a Phoenix roof insurance claim? Arizona policies require notice "as soon as practicable" after the loss. Practically, file within days of the storm — not weeks. Delayed reporting is a leading reason carriers contest claims.

What is the difference between ACV and RCV on a Phoenix roof claim? RCV pays the full replacement cost; ACV pays the depreciated value. Many Arizona carriers apply ACV to roofs older than 10–15 years, which can reduce a settlement by 50% or more on an older roof.

Can I hire any contractor to do roof repair after a Phoenix insurance claim? You should only hire a contractor licensed by the Arizona Registrar of Contractors. Unlicensed work can void your claim, prevent permitting, and eliminate your recourse if the work is defective.

What if my Phoenix roof claim is denied? You are entitled to a written denial citing specific policy provisions. You may invoke the policy's appraisal clause to dispute the amount of loss, hire a licensed public adjuster, or file a complaint with the Arizona Department of Insurance and Financial Institutions.

Next Steps for a Phoenix Roof Insurance Claim

A successful Phoenix roof insurance claim is a documentation exercise as much as a damage assessment. Photograph your roof annually, keep your declarations page where you can find it, verify your wind/hail deductible before monsoon season, and never hire an unlicensed contractor — no matter how good the storm-chaser pitch sounds. If a claim is denied or lowballed, exercise your rights under Arizona Revised Statutes Title 20: request a written explanation, invoke the appraisal clause, and file with DIFI if the carrier acts in bad faith.

Free roof inspection

Have a leak, monsoon damage, or a quote you want a second look at?

Licensed residential roofing across Phoenix and the Valley. Honest scopes, plain-language explanations, and no pressure.